Deciding between a fixed and variable mortgage rate is often the biggest hurdle homeowners face.

Whether you are a first-time buyer or a seasoned investor, the “rate-cut cycle” we’ve navigated recently has likely left you wondering where to park your money for the next few years.

At Strategic Mortgage Solutions Inc., we believe that your mortgage shouldn’t be a source of stress. It should be a tool that helps you build wealth. With over 16 years of industry experience, I have seen markets shift, interest rates skyrocket, and cycles bottom out. My goal is always to guide you through this unfamiliar territory with trustworthy leadership and bespoke mortgage solutions that keep more money in your pocket.

In this guide, we’ll break down the 2026 landscape and help you decide which path fits your unique financial goals.

The landscape has shifted: Variable rates are currently priced more aggressively than fixed rates for the first time in years, but a “plateau” in the Bank of Canada cycle means you need to weigh immediate savings against future risks.

Understanding the 2026 Rate Plateau

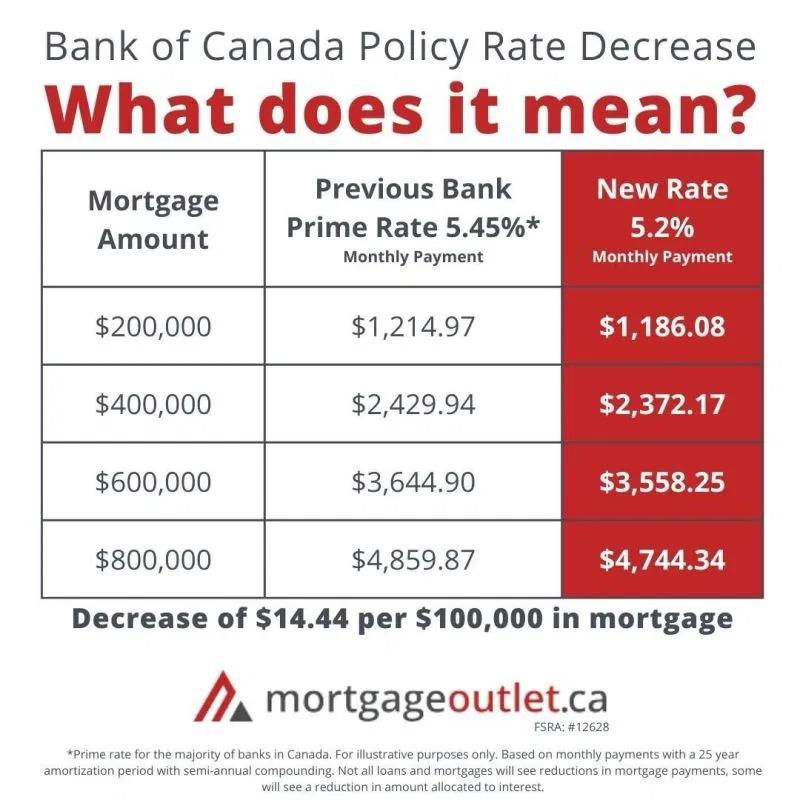

As we move through June 2026, the aggressive rate-cutting cycle of the past eighteen months has largely leveled off. The Bank of Canada has stabilized the policy rate around 2.25%, and forecasts suggest we will stay in this “plateau” phase for most of the year.

This is a unique moment. For the last decade, fixed rates were often the default “safe” choice. However, right now, we are seeing variable rates priced lower than 5-year fixed rates. When the Bank of Canada holds steady, the variable rate becomes a very attractive option because you aren’t paying a “certainty premium” to the bank.

Strategy 1: The Variable Rate Advantage

In the current market, choosing a variable rate means your interest is tied to the lender’s prime rate. Because the Bank of Canada has lowered its policy rate significantly from the highs of 2023-2024, the prime rate has followed suit.

Choose a variable rate if:

• You want lower payments today. With variable rates sitting around 3.49% (Prime minus a discount) compared to 5-year fixed rates at roughly 4.09%, the monthly savings are tangible.

• You value flexibility. Variable mortgages typically have much lower penalties to break: usually just three months of interest. This is ideal if you think you might sell your home or refinance before your five-year term is up.

• You believe rates will stay low. If you expect the Bank of Canada to hold or even trim another quarter-point, you’ll benefit immediately.

Pro Tip: If you choose a variable rate, “stress test” your own budget. Use a mortgage calculator to see what your payment would look like if rates climbed by 1%. If that number makes you sweat, you might need a different strategy.

Strategy 2: The Fixed Rate Security Blanket

Even though variable rates are currently lower, many of my clients: especially first-time homebuyers:

prefer the “sleep-at-night” factor of a fixed rate. A fixed rate stays the same for your entire term, protecting you from any surprises.

Choose a fixed rate if:

• Your budget is tight. If an extra $200 a month in interest would break your bank, locking in a rate is a smart insurance policy.

• You fear the 2027 rebound. Some economists predict that while 2026 is stable, we could see rates begin to climb again in 2027 or 2028. Locking in a 5-year fixed now protects you against that future hike.

• You want absolute predictability. You know exactly how much principal you are paying down every month, making long-term financial planning much easier.

Strategy 3: The “Wait and See” (Short-Term Fixed)

Many homeowners feel stuck. They don’t want the risk of a variable rate, but they also don’t want to lock in a 5-year fixed rate at 4.09% if they think rates might drop further in two years.

The solution? A 1-year to 3-year fixed term. This “middle ground” strategy allows you to get the certainty of a fixed payment for the near term, while giving you the opportunity to renew sooner when the market might be even more favorable. This is particularly popular for self-employed professionals who want stability while their business grows but want the option to refinance once their income history is even stronger.

Your 5-Step Action Plan

Navigating a rate-cut cycle requires more than just picking a number. It requires a strategy tailored to your life. Follow these steps to ensure you’re making the best move for your wallet:

1. Analyze your cash flow. Look at your monthly surplus. If you have plenty of room, you can afford the “risk” of a variable rate to chase higher savings.

2. Check your timeline. Are you planning to move in three years? If so, the high penalty of a 5-year fixed mortgage could cost you more than the interest savings are worth.

3. Run the numbers. Use our mortgage calculators to compare the total interest paid over 5 years for both options. Don’t just look at the monthly payment; look at the total cost of borrowing.

4. Hedge your bets. If you choose a variable rate, try making your payments as if you had the higher fixed rate. The extra money goes directly toward your principal, helping you pay off your home years sooner.

5. Get a professional second opinion. A big bank will offer you their standard products. An expert broker will look at your whole financial picture, including specialized lending solutions for credit challenged borrowers or new residents.

Why Expert Guidance Matters

At Strategic Mortgage Solutions Inc., we don’t just find you a rate; we design a plan. With 16 years of experience, I’ve helped thousands of Canadians move beyond the limitations of big banks to access a broader range of lending products that actually fit their lives.

Whether you are looking to buy, refinance, or renew, my commitment is to provide bespoke, innovative lending strategies that save you money. We take the time to explain the “why” behind the “what,” ensuring you feel confident in your homeownership journey.

Ready to see which rate strategy will save you the most? Contact us today or visit our About page to learn more about how we help Canadians optimize their mortgages. Let’s make sure your next move is your smartest one.