Are you ready for your mortgage renewal? If you’re like most Canadians, your renewal date is approaching fast. In fact, by the end of 2026, nearly 60% of all outstanding mortgages in Canada will have come up for renewal. Many of these were signed during the ultra-low rate period of 2020–2022, which means the landscape you’re walking into today looks very different than it did back then.

I’m Estee Zacks, and with over 16 years of experience in the mortgage industry, I’ve seen it all. I know that renewal season can feel like a high-stakes game of “guess the rate,” but it doesn’t have to be stressful. At Strategic Mortgage Solutions Inc., my goal is to guide you through this unfamiliar territory with bespoke solutions that actually save you money.

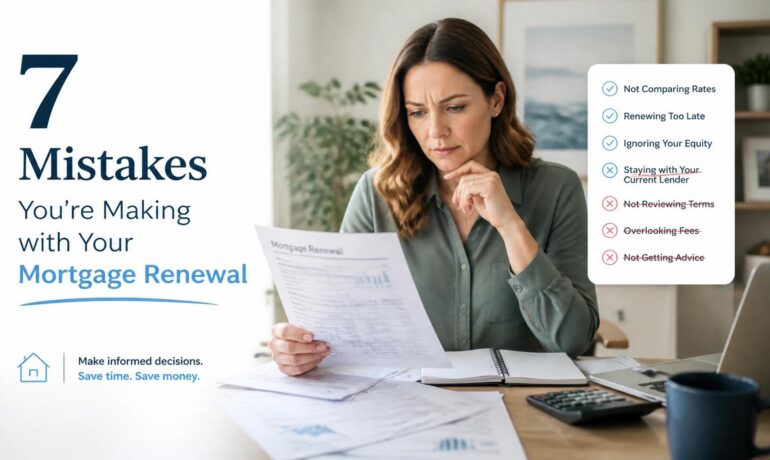

To help you get ahead of the curve, I’ve rounded up the seven biggest mistakes I see homeowners making during their renewal process: and exactly how you can avoid them.

1. Falling Into the “Inertia Trap” (Auto-Renewing)

The biggest mistake you can make is simply signing the first piece of mail your bank sends you. It’s convenient, sure. But that convenience usually comes with a massive “convenience tax.”

Banks often lead with an “okay” offer, counting on the fact that you’re too busy to shop around. They rely on your inertia. By auto-renewing, you could be leaving thousands: or even tens of thousands: of dollars on the table over the next five years.

How to fix it: Treat your renewal like a brand-new mortgage. Start by looking at what’s out there. I specialize in bespoke mortgage solutions that go beyond the big-bank limitations, giving you access to a much broader range of products and rates.

2. Waiting Until the Last Minute

If your mortgage matures in 30 days and you’re just starting to look at rates, you’ve already lost your leverage. You are now under pressure to make a decision, and the bank knows it.

How to fix it: Mark your calendar 120 to 180 days out. Most lenders allow you to lock in a renewal rate up to four months before your actual maturity date. This protects you from rate hikes while you take the time to compare your options. If rates go down before your renewal, you can usually still grab the lower one!

3. Having “Rate Blindness”

It’s easy to get obsessed with the headline interest rate. However, a “low” rate can sometimes be a trap if it comes with restrictive terms. For example, if you get a slightly lower rate but the mortgage has a high Interest Rate Differential (IRD) penalty, it could cost you $20,000 to break that mortgage early if you need to sell your home.

How to fix it: Focus on the total cost of borrowing, not just the rate. Look at prepayment privileges, portability (can you take the mortgage to a new house?), and penalty structures. Sometimes paying 0.05% more on the rate for a mortgage with better flexibility will save you much more in the long run.

4. Ignoring Your Recent Life Changes

The mortgage you signed five years ago was perfect for you then. But a lot can change in half a decade. Maybe you’re now self-employed, you’ve had another child, or you’re thinking about a major

home renovation. Renewing the exact same terms without checking if they still fit your lifestyle is a missed opportunity.

How to fix it: Audit your current financial situation. If your income has increased, you might want to increase your payment frequency or shorten your amortization. If things are tight, you might need to extend your amortization to lower your monthly payments. I help my clients align their mortgages with their five-year life plan.

5. Forgetting to Check Your “Credit Health”

Just because you already have a mortgage doesn’t mean you’ll automatically qualify for the best rates if you decide to switch lenders for a better deal. If you’ve taken on a new car loan or had a few late payments on a credit card, your credit score might have dipped.

How to fix it: Check your credit report 90 days before renewal. This gives you time to fix any errors or pay down balances to boost your score. Being “mortgage-ready” allows you to walk into negotiations with confidence. If you’re worried about your credit, don’t panic: I work with credit-challenged borrowers to find innovative lending strategies that work.

6. Going It Alone Without Expert Guidance

Many people think they only have two choices: their current bank or another big bank. This “big bank” focus limits your options to a very narrow slice of the market. You might miss out on credit unions, monoline lenders, or specialized programs that aren’t advertised to the general public.

How to fix it: Partner with a mortgage professional. Using my 16 years of experience, I do the heavy lifting for you. I track the rates, analyze the fine print, and negotiate on your behalf. Think of me as your personal advocate in the complex world of Canadian lending. We can even look at specialized programs you might not know exist.

7. Missing the Chance to Consolidate Debt

Renewal is the absolute best time to look at your “big picture” debt. If you are carrying high-interest credit card debt or a personal loan at 12% interest, why continue paying that when you could potentially wrap it into your mortgage at a much lower rate?

How to fix it: Evaluate your home equity. If you have enough equity, you can “refinance at renewal” to consolidate other debts. This can drastically improve your monthly cash flow, even if your new mortgage rate is slightly higher than your old one.

Your Renewal Action Plan: 4 Simple Steps

Ready to take control of your mortgage? Follow this simple roadmap to ensure you get the best possible deal in 2026:

1. Plan Early: Set a reminder for 6 months before your mortgage matures.

2. Get Your Paperwork Ready: Have your recent pay stubs and mortgage statement handy.

3. Review Your Goals: Are you staying in this home? Do you want to pay it off faster?

4. Consult a Professional: Reach out to me for a bespoke analysis of your situation.

The Bottom Line: A mortgage renewal isn’t just a piece of paperwork: it’s a massive financial opportunity. Don’t let it pass you by. By avoiding these common mistakes and seeking out expert advice, you can save money, reduce stress, and optimize your homeownership journey for years to come.

Ready to see what your best renewal options look like? Let’s get started today!